The preceding balance sheet for Edelweiss represented the financial condition at the noted date. But, each new transaction brings about a change in financial condition. Business activity will impact various asset, liability, and/or equity accounts without disturbing the equality of the accounting equation. How does this happen? To reveal the answer to this question, look at four specific cases for Edelweiss. See how each impacts the balance sheet without upsetting the basic equality.

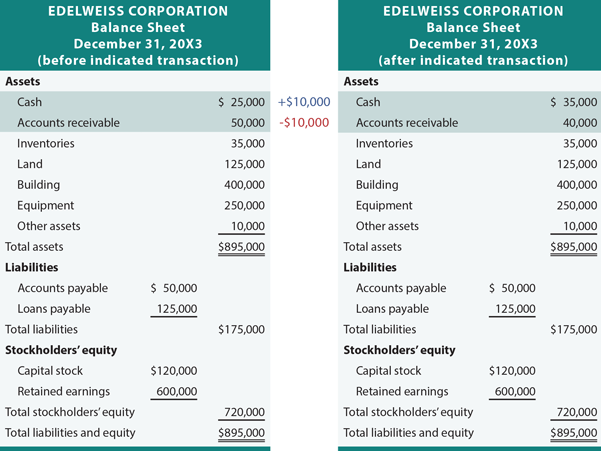

If Edelweiss Corporation collected $10,000 from a customer on an existing account receivable (i.e., not a new sale, just the collection of an amount that is due from some previous transaction), then the balance sheet would be revised to show that cash (an asset) increased from $25,000 to $35,000, and accounts receivable (an asset) decreased from $50,000 to $40,000. As a result total assets did not change, and liabilities and equity accounts were unaffected, as shown in the following illustration.

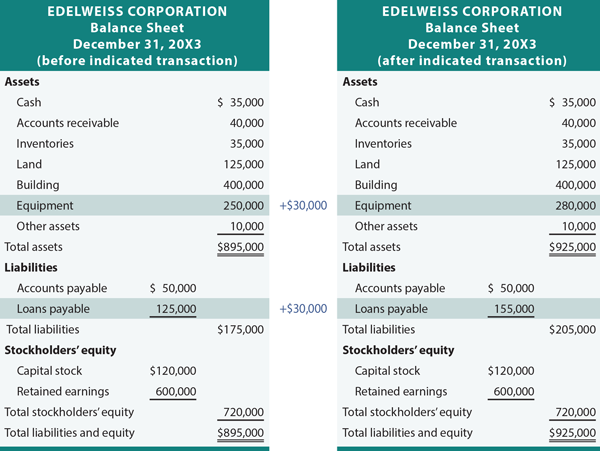

If Edelweiss Corporation purchased $30,000 of equipment, agreeing to pay for it later (i.e. taking out a loan), then the balance sheet would be further revised. The Case B illustration shows that equipment (an asset) increased from $250,000 to $280,000, and loans payable (a liability) increased from $125,000 to $155,000. As a result, both total assets and total liabilities increased by $30,000.

If Edelweiss Corporation purchased $30,000 of equipment, agreeing to pay for it later (i.e. taking out a loan), then the balance sheet would be further revised. The Case B illustration shows that equipment (an asset) increased from $250,000 to $280,000, and loans payable (a liability) increased from $125,000 to $155,000. As a result, both total assets and total liabilities increased by $30,000.

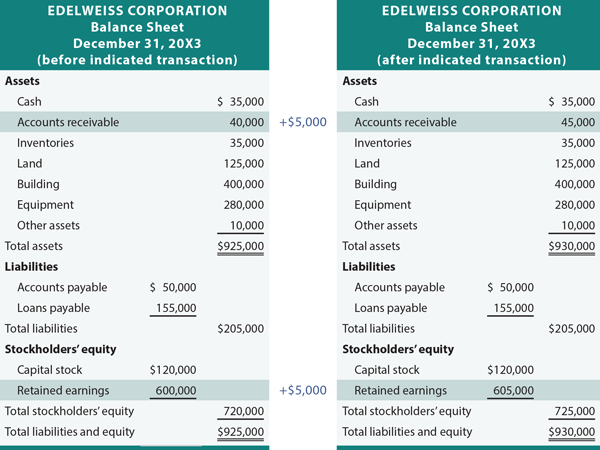

What would happen if Edelweiss Corporation did some work for a customer in exchange for the customer’s promise to pay $5,000? This requires further explanation; try to follow this logic closely! Retained earnings is the income of the business that has not been distributed to the owners of the business. When Edelweiss Corporation provided a service to a customer, it can be said that it generated revenue of $5,000. Revenue is the enhancement resulting from providing goods or services to customers. Revenue will contribute to income, and income is added to retained earnings. Examine the resulting balance sheet for Case C and notice that accounts receivable and retained earnings went up by $5,000 each, indicating that the business has more assets and more retained earnings. Note that assets still equal liabilities plus equity.

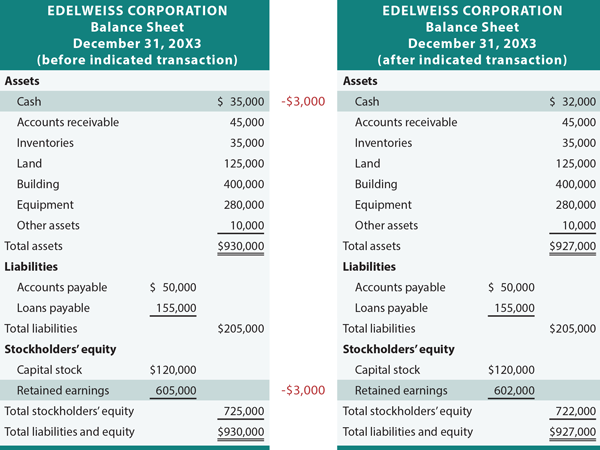

It would be nice if a business could be run without incurring any expenses. However, such is not the case. Expenses are the outflows and obligations that arise from producing goods and services. Imagine that Edelweiss paid $3,000 for expenses. This transaction reduces cash and income (i.e., retained earnings), as shown in the Case D illustration.

It would be nice if a business could be run without incurring any expenses. However, such is not the case. Expenses are the outflows and obligations that arise from producing goods and services. Imagine that Edelweiss paid $3,000 for expenses. This transaction reduces cash and income (i.e., retained earnings), as shown in the Case D illustration.

There are countless transactions, and each can be described by its impact on assets, liabilities, and equity. Importantly, no transaction will upset the balance of the accounting equation.

There are countless transactions, and each can be described by its impact on assets, liabilities, and equity. Importantly, no transaction will upset the balance of the accounting equation.

Case A: Collect An Account Receivable:

Case B: Buy Equipment via Loan:

Case C: Provide Services On Account:

Case D: Pay Expenses:

IN General

terms

In day-to-day conversation, some terms are used casually and without precision. Words may incorrectly be regarded as synonymous. Such is the case for the words “income” and “revenue.” However, each term has a very precise meaning. Revenues are enhancements resulting from providing goods and services to customers. Conversely, expenses can generally be regarded as costs of doing business. This gives rise to another accounting equation:Revenues - Expenses = Income

Revenue is the “top line” amount corresponding to the total benefits generated from business activity. Income is the “bottom line” amount that results after deducting expenses from revenue. In some countries, revenue is also referred to as “turnover.”

No comments:

Post a Comment

Thanks For Comment!!