Although every attempt is made to prepare and present financial data that are free from bias, accountants do employ a degree of conservatism. Conservatism dictates that accountants avoid overstatement of assets and income. Conversely, liabilities would tend to be presented at higher amounts in the face of uncertainty. This is not a hardened rule, just a general principle of measurement.

In the case of inventory, a company may find itself holding inventory that has an uncertain future; meaning the company does not know if or when it will sell. Obsolescence, over supply, defects, major price declines, and similar problems can contribute to uncertainty about the "realization" (conversion to cash) for inventory items. Therefore, accountants evaluate inventory and employ lower of cost or market considerations. This simply means that if inventory is carried on the accounting records at greater than its market value, a write-down from the recorded cost to the lower market value would be made. In essence, the Inventory account would be credited, and a Loss for Decline in Market value would be the offsetting debit. This debit would be reported in the income statement as a charge against (reduction in) income.

MEASURING MARKET VALUE: Market values are very subjective. In the case of inventory, applicable accounting rules define "market" as the replacement cost (not sales price!) of the goods. In other words, what would it cost for the company to acquire or reproduce the inventory?

However, the lower-of-cost-or-market rule can become complex because accounting rules specify that market not exceed a ceiling amount known as "net realizable value" (NRV = selling price minus completion and disposal costs). The reason is that "replacement cost" for some items can be very high even though there is no market in which to sell the item (e.g., out of date cell phones still in the inventory of a phone store). Such items are unlikely to produce much net value when sold. Therefore, "market" for purposes of the lower of cost or market test should not exceed the net realizable value. Additionally, the rules stipulate that "market" should not be less than a floor amount, which is the net realizable value less a normal profit margin. What arises then, is the following decision process:

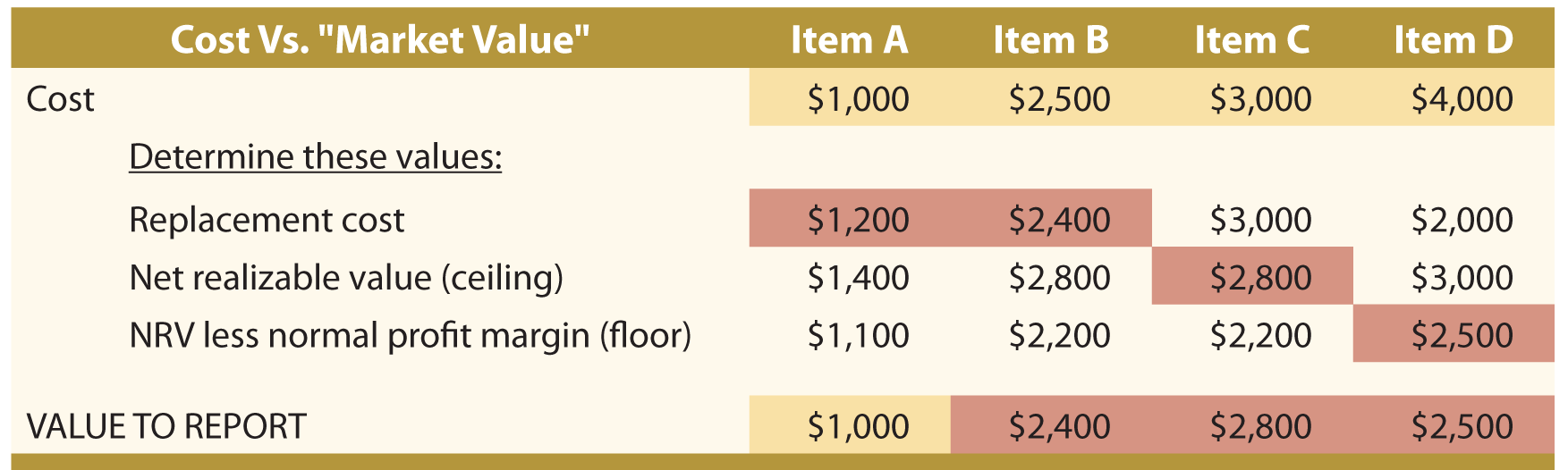

Step 1: Determine market - Replacement cost, not to exceed the ceiling nor be less than the floor.

Step 2: Report inventory at the lower of its cost or market (as determined in step 1).

To illustrate, consider the following four different inventory items, and note that the "cost" is shaded in yellow and the appropriate "market value" is shaded in red. The reported value is in the final row, and corresponds to the lower of cost or market:

APPLICATION OF LCM: Despite the apparent focus on detail, it is noteworthy that the lower-of-cost-or-market adjustments can be made for each item in inventory, or for the aggregate of all the inventory. In the latter case, the good offsets the bad, and a write-down is only needed if the overall market is less than the overall cost. In any event, once a write-down is deemed necessary, the loss should be recognized in income and inventory should be reduced. Once reduced, the Inventory account becomes the new basis for valuation and reporting purposes going forward. Write-ups of previous write-downs for any recovery in value would not be permitted under United States GAAP.

The application of lower-of-cost-or-market principles varies under IFRS (international financial reporting standards). For instance, the concepts of "ceiling and floor" are usually not applicable. Instead, the international standards speak to net realizable value as the only benchmark for assessing market. Additionally, recoveries of previous write downs are recognized under IFRS. |

No comments:

Post a Comment

Thanks For Comment!!