Of what value is accounting? Why is so much time and money spent on the development of accounting information? To fairly answer these questions, one must think broadly. Investors and creditors have limited resources and seek to place those resources where they will generate the best returns. Accounting information is the nexus of this capital allocation decision process. Without good information misallocation of capital would occur and result in inefficient production and shortages.

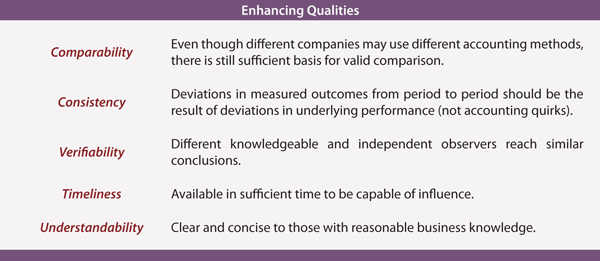

Most organizations devote a fair amount of time and effort to considering their goals and objectives. The accounting profession is no different. Foremost among the objectives of accounting and reporting is to provide useful information for investors, creditors, analysts, government, and others. Accounting information is general purpose and should be designed to serve the information needs of all types of interested parties. To be useful, information should be helpful in assessing the amounts, timing, and uncertainty of an organization’s cash flows; assist in the study of an enterprise’s resources, claims against those resources, and changes in them; and, be helpful in examining an enterprise’s financial performance. Additionally, accounting should help decision makers monitor and evaluate how well management is fulfilling its stewardship responsibilities. The following qualities help to make accounting useful.

UNDERSTANDABILITY: One challenge facing the accounting profession is to develop measurement and presentation methods that can capture and report complex business activity in a way that is understandable. Importantly, accounting reports should be comprehensible to those with a reasonable understanding of business and economic activities. It is assumed the users will study information with reasonable diligence, but it is equally presumed that those users do not need to be accounting experts.

Be aware of the growing complaint that accounting has become too complex. Many persons within and outside the profession protest the ever growing number of rules and their level of detail. The debate is generally couched under the heading “principles versus rules.” Advocates of a principles-based approach argue that general concepts should guide the judgment of individual accountants. Others argue that the world is quite complex, and accounting must necessarily be rules-based. They believe that reliance on individual judgment may lead to wide disparities in reports that could render meaningful comparisons impossible. |

No comments:

Post a Comment

Thanks For Comment!!