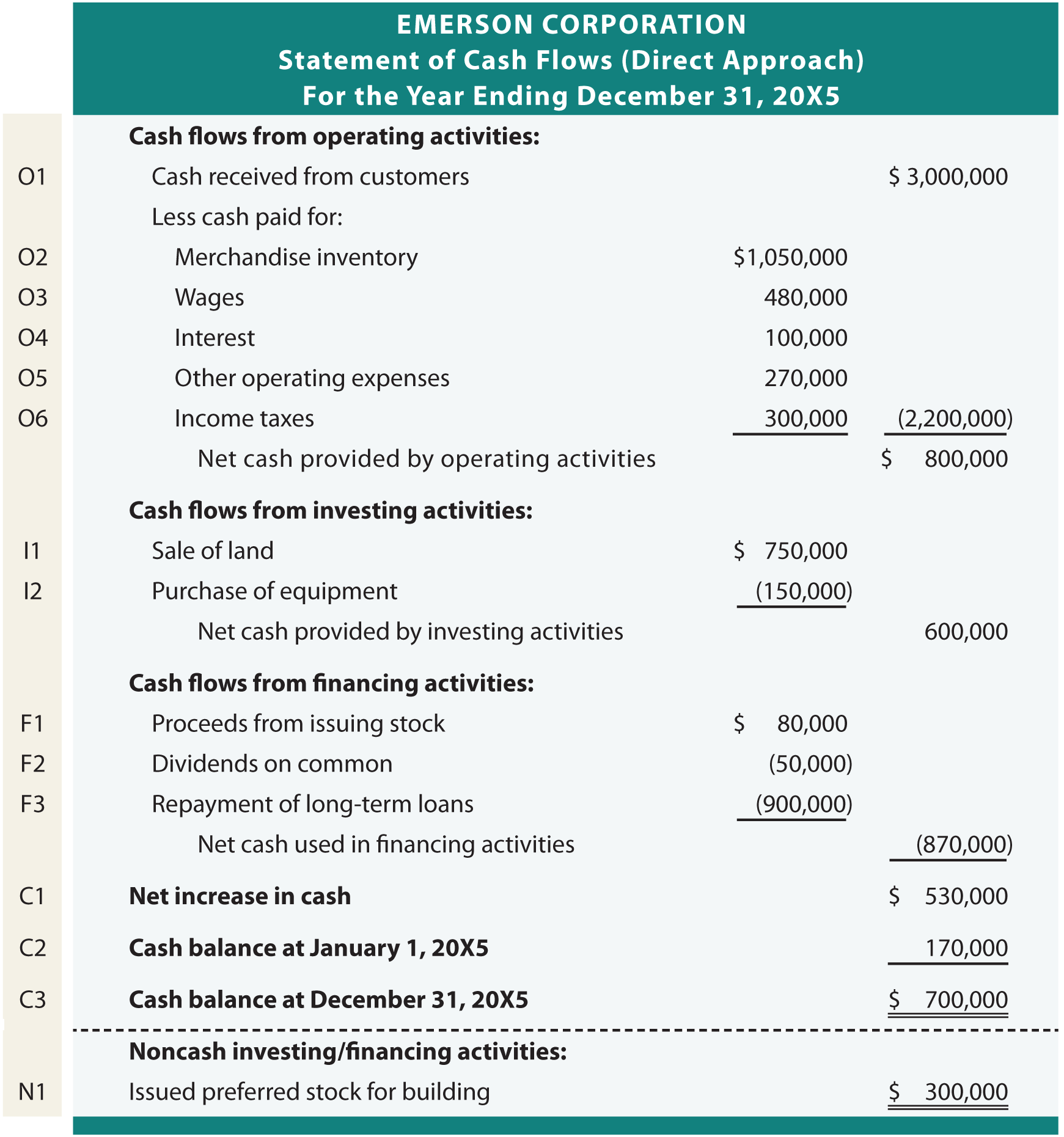

Spend just a few moments reviewing the preceding balance sheet, statement of retained earnings, and income statement for Emerson Corporation. Then, examine the following statement of cash flows. Everything within this cash flow statement is derived from the data and additional comments presented for Emerson. The tan bar on the left is not part of the statement; it is to facilitate the “line by line” explanation that follows.

OPERATING ACTIVITIES Notice that Line 01 appears as follows:

Emerson’s customers paid $3,000,000 in cash. Emerson’s information system could be sufficiently robust that a “database query” could produce this number. On the other hand, one can infer this amount by reference to sales and receivables data found on the income statement and balance sheet:

Cash Received From Customers = Total Sales Minus the Increase in Net Receivables (or, plus a decrease in net receivables) = $3,250,000 - ($850,000 - $600,000) = $3,000,000 Accounts receivable increased by $250,000 during the year ($850,000 - $600,000). This means that of the total sales of $3,250,000, a net $250,000 went uncollected. Thus, cash received from customers was $3,000,000. If net receivables had decreased, cash collected would have exceeded sales.

Emerson paid $1,050,000 of cash for inventory. Bear in mind that cost of goods sold is the dollar amount of inventory sold. But, the amount of inventory actually purchased will be less than this amount if inventory on the balance sheet decreased. This would mean that some of the cost of goods sold came from existing stock on hand rather than having all been purchased during the year. On the other hand, purchases would be greater than cost of goods sold if inventory increased.

Inventory Purchased = Cost of Goods Sold Minus the Decrease in Inventory (or, plus an increase in inventory) = $1,160,000 - ($220,000 - $180,000) = $1,120,000 Inventory purchased is only the starting point for determining cash paid for inventory. Inventory purchased must be adjusted for the portion that was purchased on credit. Notice that Emerson’s accounts payable increased by $70,000 ($270,000 - $200,000). This means that cash paid for inventory purchases was $70,000 less than total inventory purchased:

Cash Paid for Inventory = Inventory Purchased Minus the Increase in Accounts Payable (or, plus a decrease in accounts payable) = $1,120,000 - ($270,000 - $200,000) = $1,050,000

Emerson paid $480,000 of cash for wages during the year. Emerson’s payroll records would indicate the amount of cash paid for wages, but this number can also be determined by reference to wages expense in the income statement and wages payable on the balance she

Cash Paid for Wages = Wages Expense Plus the Decrease in Wages Payable (or, minus an increase in wages payable) = $450,000 + ($50,000 - $20,000) = $480,000 Emerson not only paid out enough cash to cover wages expense, but an additional $30,000 as reflected by the overall decrease in wages payable. If wages payable had increased, the cash paid would have been less than wages expense.

Emerson’s cash payments for these items equaled the amount of expense in the income statement. Had there been related balance sheet accounts (e.g., interest payable, taxes payable, etc.), then the expense amounts would need to be adjusted in a manner similar to that illustrated for wages.

Overall, operations generated net positive cash flows of $800,000. Notice that two items within the income statement were not listed in the operating activities section of the cash flow statement:

- Depreciation is not an operating cash flow item. It is a noncash expense. Remember that depreciation is recorded via a debit to Deprecation Expense and a credit to Accumulated Depreciation. No cash is impacted by this entry (the “investing” cash outflow occurred when the asset was purchased), and

- The gain on sale of land in the income statement does not appear in the operating cash flows section. While the land sale may have produced cash, the entire proceeds will be listed in the investing activities section; it is a “nonoperating” item.

INVESTING ACTIVITIES: The next major section of the cash flow statement is the cash flows from investing activities. This section can include both inflows and outflows related to investment-related transactions. Emerson Corporation had one example of each; a cash inflow from sale of land, and a cash outflow for the purchase of equipment. The sale of land requires some thoughtful analysis.

Notice that the statement of cash flows for Emerson reports the following line item:

This line item reports that $750,000 of cash was received from the sale of land during the year. In actuality, it would be possible to look up this transaction in the company’s journal. That entry would appear as follows:

But, it is not necessary to refer to the journal. Notice that land on the balance sheet decreased by $600,000 ($1,400,000 - $800,000), and that the income statement included a $150,000 gain. Applying a little “forensic” accounting allows one to deduce that $600,000 in land was sold for $750,000, to produce the $150,000 gain.

Emerson purchased equipment for $150,000 during the year. Notice that equipment on the balance sheet increased by $150,000 ($1,050,000 - $900,000). One could confirm that this was a cash purchase by reference to the journal; such is assumed in this case.

FINANCING ACTIVITIES:

This line reveals that $80,000 was received from issuing common stock. This cash inflow is suggested by the $10,000 increase in common stock ($910,000 - $900,000) and $70,000 increase in additional paid-in capital ($370,000 - $300,000).

The statement of retained earnings reveals that Emerson declared $50,000 in dividends. Since there is no dividend payable on the balance sheet, one can assume that all of the dividends were paid.

The balance sheet reveals a $900,000 decrease in long-term debt ($1,800,000 - $900,000). This represented a significant use of cash.

CASH FLOW RECAP

Emerson had a $530,000 increase in cash during the year ($800,000 from positive operating cash flow, $600,000 from positive investing cash flow, and $870,000 from negative financing cash flow). This change in cash is confirmed by reference to the beginning and ending cash balances.

NONCASH INVESTING/FINANCING ACTIVITIES

The noncash investing and financing section reports that preferred stock was issued for a building.

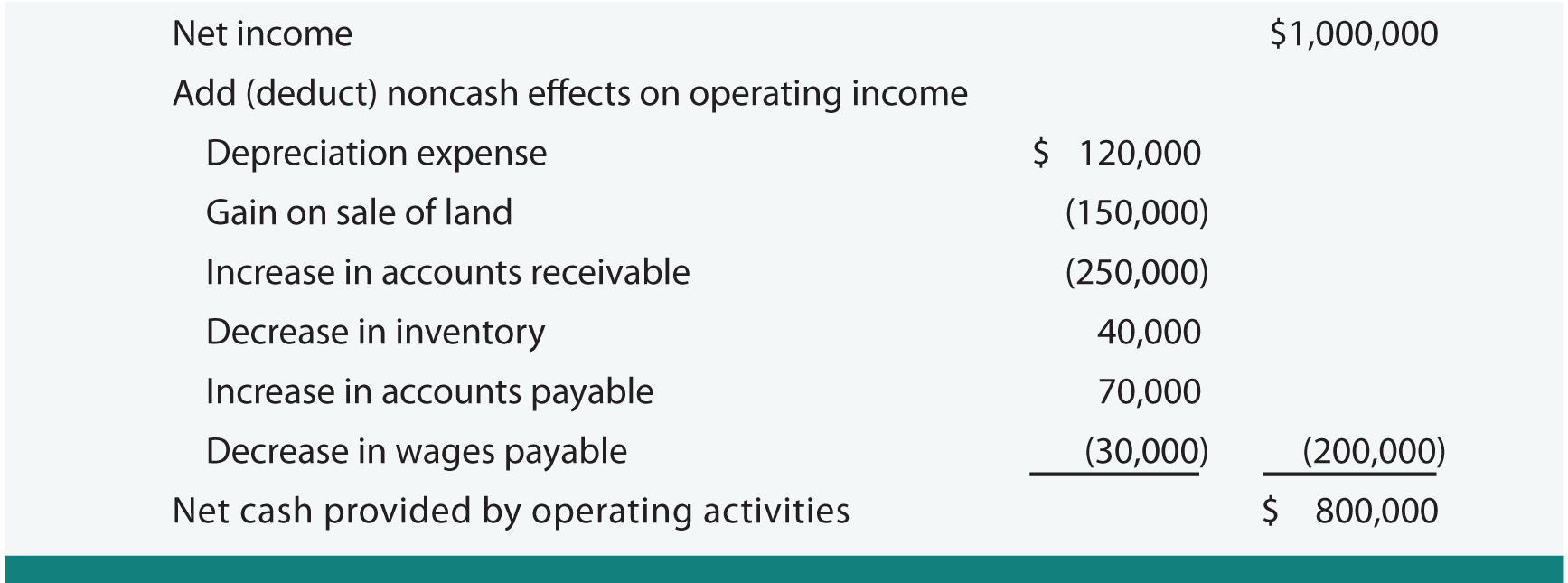

RECONCILIATION The statement of cash flows just presented is known as the “direct approach.” It is so named because the cash items entering into the determination of operating cash flow are specifically identified. In many respects, this presentation of operating cash flows resembles a cash basis income statement. An acceptable alternative is the “indirect” approach. Before moving on to the indirect approach, be aware that companies using the direct approach must supplement the cash flow statement with a reconciliation of income to cash from operations. This reconciliation may be found in notes accompanying the financial statements:

Notice that this reconciliation starts with the net income, and adjusts to the $800,000 net cash from operations. Some explanation may prove helpful:

- Depreciation is added back to net income, because it reduced income but did not consume any cash.

- Gain on sale of land is subtracted, because it increased income, but is not related to operations (remember, it is an investing item and the “gain” is not the sales price).

- Increase in accounts receivable is subtracted, because it represents uncollected sales included in income.

- Decrease in inventory is added, because it represents cost of sales from existing inventory (not a new cash purchase).

- Increase in accounts payable is added, because it represents expenses not paid.

- Decrease in wages payable is subtracted, because it represents a cash payment for something expensed in an earlier period.

This can become rather confusing. Most can probably see why depreciation is added back. But, the gain may be fuzzy. It must be subtracted because one is trying to remove it from the operating number; it increased net income, but it is viewed as something other than operating, and that is why it is backed out. Conversely, a loss on such a transaction would be added.

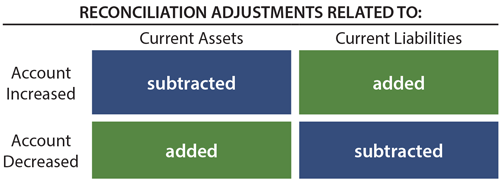

The following drawing is useful in simplifying consideration of how changes in current assets and current liabilities result in reconciliations of net income to operating cash flows. Begin by thinking about a reconciling item that is fairly easy to grasp. Emerson’s accounts receivable increased on the balance sheet, but the amount of the increase was subtracted in the reconciliation (again, this increase reflects sales not yet collected in cash, and thus the subtracting effect). In the drawing below, consider that accounts receivable is a current asset, and it increased. This condition relates to the upper left quadrant; hence the increase is shown as “subtracted.”

Using the accounts receivable analysis as a benchmark, it then becomes logical that all increasing current assets result in subtractions in the reconciliation. This relationship is inversed for current liabilities, as shown in the upper right quadrant of the drawing. Similarly, these relationships are further inversed for account decreases as shown in the bottom half of the drawing. With the drawing it mind, it becomes a simple matter to examine changes in specific current accounts to determine whether they are generally added or subtracted in the reconciliation of net income to cash flows from operating activities.

|

No comments:

Post a Comment

Thanks For Comment!!