Having established that an allowance method for uncollectibles is preferable (indeed, required in many cases), it is time to focus on the details. Begin with a consideration of the balance sheet. Suppose that Ito Company has total accounts receivable of $425,000 at the end of the year, and is in the process or preparing a balance sheet. Obviously, the $425,000 would be reported as a current asset. But, what if it is estimated that $25,500 of this amount may ultimately prove to be uncollectible? Thus, a more correct balance sheet presentation would show the total receivables along with an allowance account (which is a contra asset account) that reduces the receivables to the amount expected to be collected. This anticipated amount is often termed the net realizable value.

DETERMINE THE ALLOWANCE ACCOUNT: In the preceding illustration, the $25,500 was simply given as part of the fact situation. But, how would such an amount actually be determined? If Ito Company's management knew which accounts were likely to not be collectible, they would have avoided selling to those customers in the first place. Instead, the $25,500 simply relates to the balance as a whole. It is likely based on past experience, but it is only an estimate. It could have been determined by one of the following techniques:

- AS A PERCENTAGE OF TOTAL RECEIVABLES: Some companies anticipate that a certain percentage of outstanding receivables will prove uncollectible. In Ito's case, maybe 6% ($425,000 x 6% = $25,500).

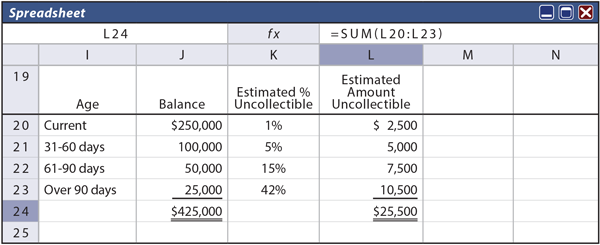

- VIA AN AGING ANALYSIS: Other companies employ more sophisticated aging of accounts receivable analysis. They will stratify the receivables according to how long they have been outstanding (i.e., perform an aging), and apply alternative percentages to the different strata. Obviously, the older the account, the more likely it is to represent a bad account. Ito's aging may have appeared as follows:

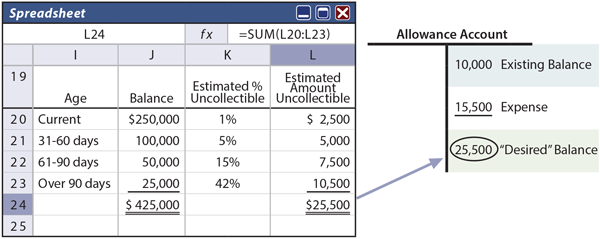

Both the percentage of total receivables and the aging are termed "balance sheet approaches." In both cases, the allowance is determined by an analysis of the outstanding accounts receivable. Once the estimated amount for the allowance account is determined, a journal entry will be needed to bring the ledger into agreement. Assume that Ito's ledger revealed an Allowance for Uncollectible Accounts credit balance of $10,000 (prior to performing the above analysis). As a result of the analysis, it can be seen that a target balance of $25,500 is needed; necessitating the following adjusting entry:

Carefully study the illustration that follows. It should be helpful in comprehending the balance sheet approaches. In particular take note of two important concepts:

- with balance sheet approaches, the amount of the entry is based upon the needed change in the account (i.e., to go from an existing balance to the balance sheet target amount), and

- the debit is to an expense account, reflecting the added cost associated with the additional amount of anticipated bad debts.

Balance Sheet Approaches

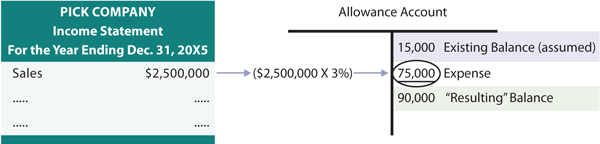

Rather than implement a balance sheet approach as above, some companies may follow a simpler income statement approach. With this equally acceptable allowance technique, an estimated percentage of sales (or credit sales) is simply debited to Uncollectible Accounts Expense and credited to the Allowance for Uncollectible Accounts each period. Importantly, this technique merely adds the estimated amount to the Allowance account. To illustrate, assume that Pick Company had sales during the year of $2,500,000, and it records estimated uncollectible accounts at a rate of 3% of total sales. Therefore, the appropriate entry to record bad debts cost is as follows:

This entry would be the same even if there was already a balance in the allowance account. In other words, the income statement approach adds the calculated increment to the allowance, no matter how much may already be in the account from prior periods.

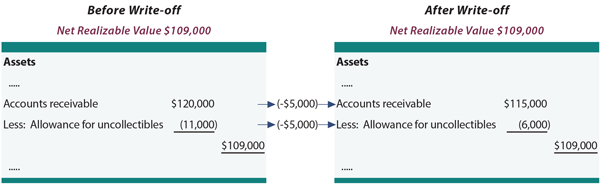

Income Statement Approaches WRITING OFF ACCOUNTS: When an allowance method is used, how are individual accounts written off? The following entry would be needed to write off a specific account that is finally deemed uncollectible:

Notice that the entry reduces both the allowance account and the related receivable, and has no impact on the income statement. Further, consider that the write-off has no impact on the net realizable value of receivables, as shown by the following illustration of a $5,000 write-off:

ACCOUNTS PREVIOUSLY WRITTEN OFF: On occasion, a company may collect an account that was previously written off. For example, a customer that was once in dire financial condition may recover, and unexpectedly pay an amount that was previously written off. The entry to record the recovery involves two steps: (1) a reversal of the entry that was made to write off the account, and (2) recording the cash collection on the account:

It may seem incorrect for the allowance account to be increased because of the above entries, but the general idea is that another as yet unidentified account may prove uncollectible (consistent with the overall estimates in use). If this does not eventually prove to be true, an adjustment of the overall estimation rates may be indicated.

MATCHING ACHIEVED: Carefully consider that the allowance methods all result in the recording of estimated bad debts expense during the same time periods as the related credit sales. These approaches satisfy the desired matching of revenues and expenses.

MONITORING AND MANAGING ACCOUNTS RECEIVABLE: A business must carefully monitor its accounts receivable. This chapter has devoted much attention to accounting for bad debts; but, don't forget that it is more important to try to avoid bad debts by carefully monitoring credit policies. A business should carefully consider the credit history of a potential credit customer, and be certain that good business practices are not abandoned in the zeal to make sales. It is customary to gather this information by getting a credit application from a customer, checking out credit references, obtaining reports from credit bureaus, and similar measures. Oftentimes, it becomes necessary to secure payment in advance or receive some other substantial guaranty such as a letter of credit from an independent bank. All of these steps are normal business practices, and no apologies are needed for making inquiries into the creditworthiness of potential customers. Many countries have very liberal laws that make it difficult to enforce collection on customers who decide not to pay or use "legal maneuvers" to escape their obligations. As a result, businesses must be very careful in selecting parties that are allowed trade credit in the normal course of business.

Equally important is to monitor the rate of collection. Many businesses have substantial dollars tied up in receivables, and corporate liquidity can be adversely impacted if receivables are not actively managed to insure timely collection. One ratio that is often monitored is the accounts receivable turnover ratio. That number reveals how many times a firm's receivables are converted to cash during the year. It is calculated as net credit sales divided by average net accounts receivable:

Accounts Receivable Turnover Ratio = Net Credit Sales / Average Net Accounts Receivable To illustrate these calculations, assume Shoztic Corporation had annual net credit sales of $3,000,000, beginning accounts receivable (net of uncollectibles) of $250,000, and ending accounts receivable (net of uncollectibles) of $350,000. Shoztic's average net accounts receivable is $300,000 (($250,000 + $350,000)/2), and the turnover ratio is "10":

10 = $3,000,000 / $300,000 A closely related ratio is the "days outstanding" ratio. It reveals how many days sales are carried in the receivables category:

Days Outstanding = 365 Days / Accounts Receivable Turnover Ratio For Shoztic, the days outstanding calculation is:

36.5 = 365 / 10 By themselves, these numbers mean little. But, when compared to industry trends and prior years, they will reveal important signals about how well receivables are being managed. In addition, the calculations may provide an "early warning" sign of potential problems in receivables management and rising bad debt risks. Analysts carefully monitor the days outstanding numbers for signs of weakening business conditions. One of the first signs of a business downturn is a delay in the payment cycle. These delays tend to have ripple effects; if a company has trouble collecting its receivables, it won't be long before it may have trouble paying its own obligations. |

No comments:

Post a Comment

Thanks For Comment!!