A written promise from a client or customer to pay a definite amount of money on a specific future date is called a note receivable. Such notes can arise from a variety of circumstances, not the least of which is when credit is extended to a new customer with no formal prior credit history. The lender uses the note to make the loan more formal and enforceable. Such notes typically bear interest charges. The maker of the note is the party promising to make payment, the payee is the party to whom payment will be made, the principal is the stated amount of the note, and the maturity date is the day the note will be due.

Interest is the charge imposed on the borrower of funds for the use of money. The specific amount of interest depends on the size, rate, and duration of the note. In mathematical form interest equals Principal x Rate x Time. For example, a $1,000, 60-day note, bearing interest at 12% per year, would result in interest of $20 ($1,000 x 12% x 60/360). In this calculation, notice that the "time" was 60 days out of a 360 day year. Obviously, a year normally has 365 days, so the fraction could have been 60/365. But, for simplicity, it is not uncommon for the interest calculation to be based on a presumed 360-day year or 30-day month. This presumption probably has its roots in olden days before electronic calculators, as the resulting interest calculations are much easier. But, with today's technology, there is little practical use for the 360 day year, except that it tends to benefit the creditor by producing a little higher interest amount -- caveat emptor (Latin for "let the buyer beware")! The following illustrations will preserve this approach with the goal of producing nice round numbers that are easy to follow.

ACCOUNTING FOR NOTES RECEIVABLE: To illustrate the accounting for a note receivable, assume that Butchko initially sold $10,000 of merchandise on account to Hewlett. Hewlett later requested more time to pay, and agreed to give a formal three-month note bearing interest at 12% per year. The entry to record the conversion of the account receivable to a formal note is as follows:

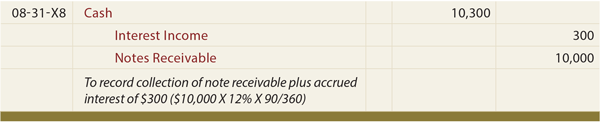

At maturity, Butchko's entry to record collection of the maturity value would appear as follows:

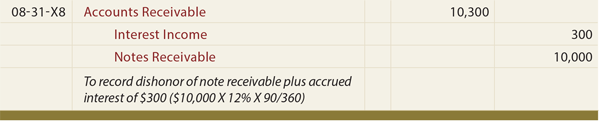

Dishonored Note: If Hewlett dishonored the note at maturity (i.e., refused to pay), then Butchko would prepare the following entry:

The debit to Accounts Receivable reflects the hope of eventually collecting all amounts due, including interest. If Butchko anticipated difficulty collecting the receivable, appropriate allowances would be established in a fashion similar to those illustrated earlier in the chapter.

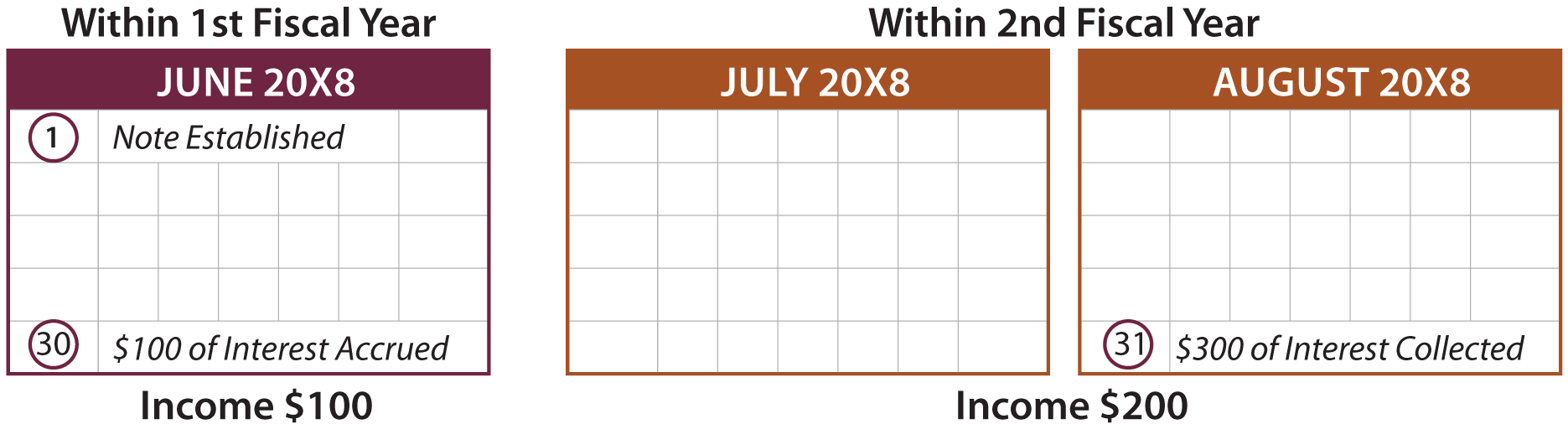

NOTES AND ADJUSTING ENTRIES: In the illustrations for Butchko, all of the activity occurred within the same accounting year. However, if Butchko had a June 30 accounting year end, then an adjustment would be needed to reflect accrued interest at year-end. The appropriate entries illustrate this important accrual concept:

Entry to set up note receivable:

Entry to accrue interest at June 30 year end:

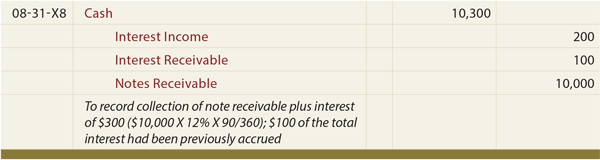

Entry to record collection of note (including amounts previously accrued at June 30):

The following drawing should aid one's understanding of these entries:

|

No comments:

Post a Comment

Thanks For Comment!!